Mandatory e-invoicing in Germany: Abacus is ready - are you?

• minutes reading time

What is behind the legal obligation for e-invoicing in Germany?

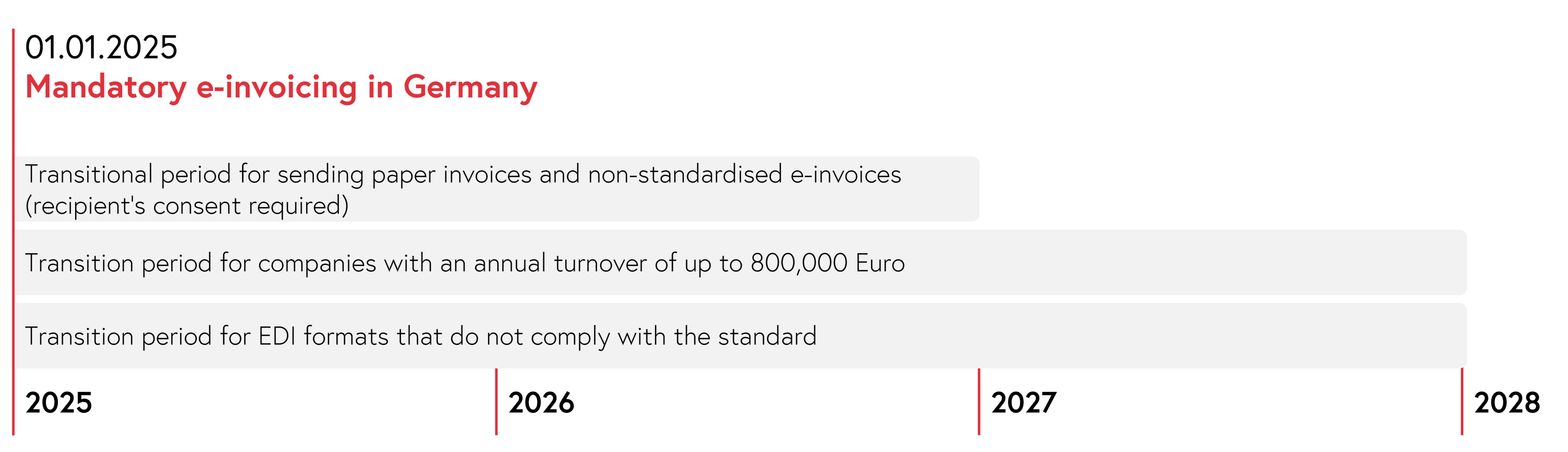

From 1 January 2025, the electronic receipt of invoices in business transactions between companies will be mandatory in Germany. Essentially, the e-invoice obligation requires invoices to be issued, transmitted and received in a structured electronic format, which enables automatic processing. These include formats such as ZUGFeRD, XRechnung and similar standards that are compatible with the European standard EN 16931. This standard ensures the interoperability of invoice data at national and European level. Conventional PDF invoices do not comply with this standard.

It will still be possible to send and receive paper invoices or e-invoices in various formats until 31 December 2026. However, it should be noted that paper invoices are no longer favoured and the recipient is obliged to accept an e-invoice. For electronic formats that are not EN 16931-compliant, such as PDF documents, the explicit consent of the recipient must still be obtained. Until 31 December 2027, companies with an annual turnover of less than 800,000 Euro can benefit from a special regulation that gives them more time to implement the necessary adjustments. Electronic Data Interchange (EDI) is also permitted after 2027, provided the format is EN 16931-compliant and compatible. This is the case with the EDIFACT format, for example. Companies that do not use a legally compliant EDI format will be granted a transitional period until 31 December 2027 to make the necessary adjustments.

The e-invoicing obligation does not stipulate a transmission channel. They can also be sent by e-mail, provided the format conforms to the standard.

Who is affected by this obligation?

The obligation to e-invoice applies to all companies (invoice issuers and invoice recipients) with a registered office or branch in Germany that are active in the B2B sector. A purely VAT registration in Germany without a branch does not constitute an obligation to e-invoice. This applies to large companies as well as small and medium-sized enterprises. Invoices up to an amount of 250 Euro and certain tax-free services in accordance with the Value Added Tax Act are exempt from this obligation.

What will change for Swiss companies?

The following changes apply to Swiss companies that maintain business relationships with German companies:

Swiss companies with branches in Germany are therefore advised to review their invoicing processes and adapt them if necessary in order to fulfil the new requirements and ensure smooth business transactions with German partners.

What will happen in the EU and Switzerland?

As part of the "VAT in the Digital Age" (ViDA) initiative, the European Union is planning the gradual introduction of a cross-border electronic reporting system for invoices within the EU. However, as a non-EU member, this system only affects Switzerland indirectly.

In future, Switzerland could introduce its own regulations on electronic invoicing in B2B business in order to simplify cross-border trade and strengthen the digital single market. However, there is currently no general obligation to accept and send electronic invoices.

With Abacus you are ready for the e-invoicing obligation

In the Abacus Business Software there are various options for sending or receiving electronic invoices.

Process e-invoices with Abacus E-Business

Sending and receiving electronic invoices is possible without restriction with the e-business application. The e-invoices received are then processed further in Accounts Payable. The e-invoice formats ZUGFeRD, XRechnung and Factur-X are supported. Abacus supports all formats that comply with the EN 16931 standard and will continue to develop the product range in a future-oriented manner and in line with regulatory requirements.

Process e-invoices with DeepBox and AbaScan Pro

The receipt of vendor invoices is also possible via DeepBox or AbaScan Pro. Various formats that comply with the EN 16931 standard are also supported in this way.

Questions? We are here for you!

If you need support or have questions about invoice processing with Abacus, our experts will be happy to help you.